Market review Q2 2026

Macro-Economic Overview

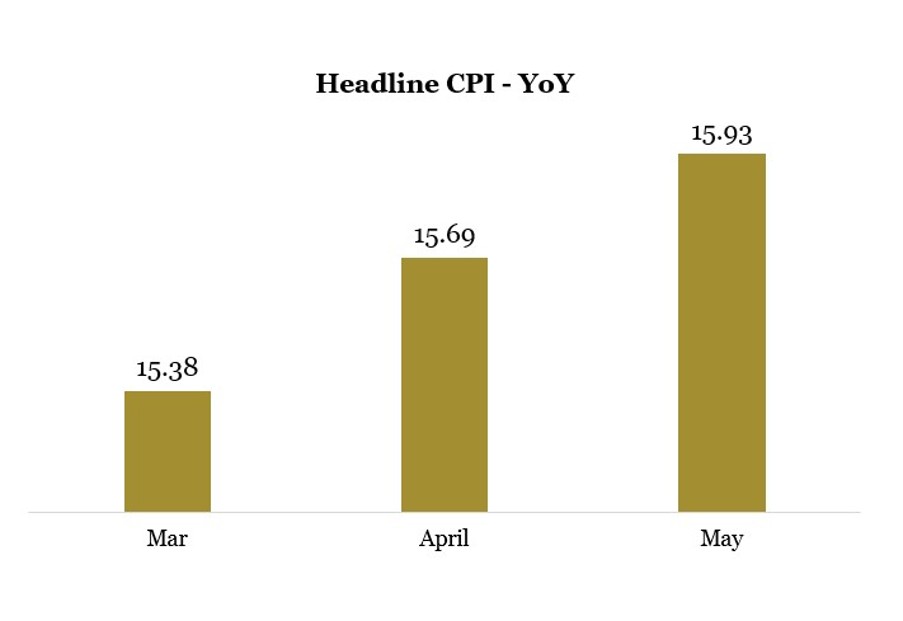

Headline inflation rose steadily throughout Q2 2026, increasing from 15.69% in April to 15.93% YoY in May. The uptick was largely driven by higher transportation and energy costs stemming from the Middle East conflict, which also filtered through to food prices. However, the month-on-month (MoM) inflation trend told a slightly different story, easing from 2.13% in April to 1.75% in May, reflecting a moderation in sequential price pressures in May amid easing geopolitical tensions.

At the Monetary Policy Committee (MPC) meeting held on 19th and 20th of May, the Committee retained the Monetary Policy Rate (MPR) at 26.50%, while maintaining the Standing Facilities Corridor at +50/-450 basis points around the MPR. The Cash Reserve Ratio (CRR) was also left unchanged at 45% for Deposit Money Banks, 16% for Merchant Banks, and 75% for non-TSA public sector deposits.

Crude oil prices remained highly volatile in Q2 2026, largely reflecting geopolitical developments in the Middle East. Brent crude averaged approximately $96.01/barrel during the quarter, trading between a low of $72.60/barrel and a high of over $120/barrel. Prices surged sharply in April amid supply disruption fears linked to tensions around the Strait of Hormuz but moderated through May and June as supply conditions improved and ceasefire efforts gained traction.

Nigeria’s Composite PMI weakened during Q2 2026, declining from 53.2 points in March to 49.4 points in April before printing at 49.6 points in May. This signals a second consecutive month of contraction in business activity after 16 months of expansion. This can be largely attributed to weaker activity in the industrial and services sectors.

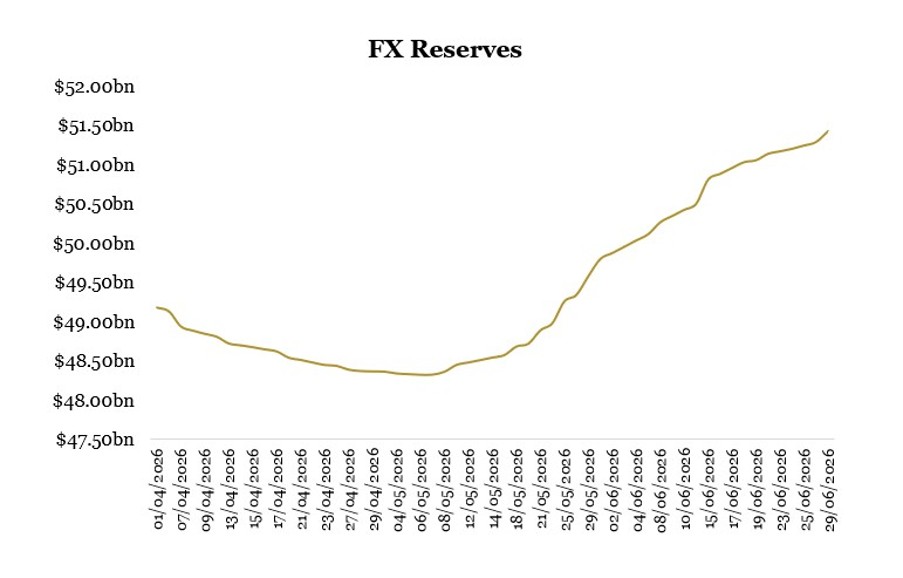

As of 29 June 2026, Nigeria’s gross external reserves stood at $51.43 billion, representing a 4.45% increase from the $49.24 billion recorded as of 31 March 2026.

The total FAAC disbursement in Q2 so far amounted to approximately ₦2.13 trillion.

Interbank liquidity remained robust during the quarter, averaging approximately ₦4.84 trillion, peaking at around ₦7.78 trillion in late April and dipping to approximately ₦2.57 trillion in mid-June.

Sources: FMDQ, CBN, NBS, Bloomberg

Bond market

The FGN bond market experienced a notable shift in sentiment during Q2 2026 as investors reassessed the outlook for interest rates and the government’s borrowing plans. Trading remained largely selective throughout the quarter, with the secondary market alternating between bargain hunting and profit-taking as investors searched for attractive entry levels. Yields remained broadly range-bound through the early part of the quarter as market participants cautiously positioned ahead of fresh supply. Although demand at the April auction was robust, the DMO maintained its disciplined stance, allotting only ₦276.8bn of the ₦700bn offered across the 2030s, 2032s, and 2035s, closing at 16.30%, 16.50%, and 16.59%, respectively. The restrained allotment helped keep yields relatively anchored despite healthy investor demand. In May, the DMO reopened the 2035s and 2037s, closing at 17.00% and 17.04%, respectively, signalling the beginning of an upward adjustment in market yields and setting the tone for a broader repricing in June.

The market turned more bearish towards the end of the quarter as increased sovereign issuance prompted investors to demand higher yields. Selling pressure emerged across the curve ahead of the June auction, pushing yields upward before demand resurfaced at the new levels. The DMO offered ₦1.20tn across the 2035s and 2037s, attracting subscriptions of over ₦1.41tn and allotting ₦1.22tn at marginal rates of 18.34% and 18.35%, respectively. The uptick in rates from the previous month underscores the market’s repricing of sovereign risk, as investors sought greater compensation to absorb the significantly larger supply of government debt.

Treasury Bill market

The Nigeria Treasury bills market recorded mixed performance in Q2 2026, as the strong liquidity driven bullish bias witnessed at the start of the quarter gradually gave way to a more cautious trading environment. While the robust market liquidity and investor demand compressed yields, the inflationary pressures, heightened geopolitical tensions in the Middle East and the Monetary Policy Committee’s decision to maintain a hawkish stance ultimately shifted market sentiments further in the quarter.

In April, the ample liquidity drove strong demand, particularly on the short-term bills, as investors sought to preserve portfolio flexibility amid the uncertain economic environment. The bullish run compressed secondary market yields, while the Primary Market Auctions (PMAs) attracted over c. ₦5.30 trillion in subscription, signaling a healthy investor appetite. Market sentiments moderate in May, as inflation rose to 15.69% from 15.38%, coupled with the heightened US-Iran tensions reinforced expectations of a resistant monetary policy environment. Mid-month the MPC met and MPR was maintained at 26.50%, driving average yields to decline marginally by 6bps in May. The Marker was repriced sharply in June following the significant increase in both CBN and DMO issuance. The DMO revised its quarterly NTB issuance from ₦3.95trn to ₦4.80trn, with both June auctions receiving larger offer sizes of ₦1.00trn from ₦700bn and ₦450bn respectively. At the final NTB auction of the quarter (17-Jun), we saw allotments increase further to ₦1.49trn, with stop rates climbing sharply to 16.28%, 16.50% and 17.34%, respectively.

The higher Primary market Stop rates triggered a broad repricing in the secondary market, driving yields higher across the curve. Consequently, the benchmark 1-year NTB closed the quarter c. 21.00% yield.

The CBN floated seventeen (17) OMO auctions during the quarter, offering c. ₦10.20 trn across the tenors. Total sales during the quarter over c. ₦32.00 trn. Despite the oversubscriptions recorded at the auctions, there were two (2) no sale during the auctions.

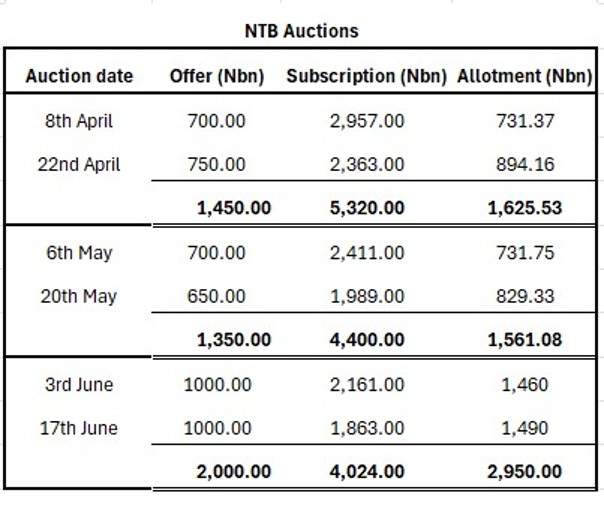

The DMO conducted six (6) NTB auctions during the quarter with each month recording an oversubscription of ₦5.32 trn, ₦4.40 trn and ₦4.02 trn respectively. In total the DMO oversold N1.34 trn, by allotting N6.14trn against the N4.80trn on offer.

Eurobond Market

Global macro conditions remained mixed during the second quarter of 2026. Major central banks paused their aggressive tightening cycles. The Federal Reserve maintained its funds rate at 3.50% to 3.75%, while the European Central Bank held rates before raising its deposit rate to 2.25% in June. Energy markets saw high volatility; Brent crude spiked to 118 dollars in April amid Middle East conflict before retreating to the 70 to 80 dollar range by late June. China’s manufacturing PMI hovered around the 50-point expansion threshold, limiting export momentum for emerging markets. In this environment, Sub-Saharan African Eurobond markets saw stable to slightly firmer conditions. Yield curves flattened modestly, carry trades in belly maturities were highly favoured, and primary issuance continued selectively with solid investor demand. Regional trends featured steady disinflation and improved foreign exchange reserves.

Global Economic & Market Backdrop

The second quarter delivered diverging signals for global risk assets. Fixed income yields in the United States and Europe largely plateaued. The Federal Reserve held interest rates steady throughout May and June, choosing not to cut, while the ECB delivered a modest 25 basis point hike in mid-June. The dollar traded within a narrow horizontal band, with the dollar index hovering between 100 and 102. The Fed’s commitment to a higher-for-longer stance kept frontier market yields highly attractive to international investors. Oil prices spiked sharply due to geopolitical conflicts, lifting Brent crude by roughly 60% by late April before a sharp correction occurred in June during ceasefire discussions. China’s weak manufacturing data kept general emerging market risk appetite muted. Investors chose to lock in high yields in sovereign debt, and the JPM EMBIG Sub-Saharan index ended the quarter flat to tighter, with high-quality credits outperforming. Most market activity focused on liability management, such as bond buybacks and targeted paper re-openings, rather than large new sovereign debt sales.

- Global Central Banks and Commodities: The Fed paused in April and June, while futures markets priced in just one rate cut for 2026. The ECB hiked by 25 basis points in June after an April pause. Brent crude spiked to 118 dollars before sliding down to 77 dollars by late June as geopolitical conflicts calmed down. The US dollar remained stable, easing slightly by the end of June on broad profit-taking.

- Sub-Saharan Africa Technicals: Sub-Saharan Eurobonds gained from this renewed risk-on sentiment. JPM EMBI spreads finished flat to slightly tighter, though higher-yielding credits underperformed. The primary market saw successful new issuances from Angola, Egypt, Cameroon, and Kenya. Secondary market yield curves flattened as sovereign funding anxieties dissipated. Portfolio inflows remained supported by ongoing IMF and World Bank programs alongside steady external financing arrangements. Cash bonds in the 5-to-10-year belly segment clearly outperformed longer maturities, showing a clear investor preference for high carry over long duration. Market liquidity stayed ample, and front-end yields were anchored by spare oil production capacity. Investor interest gravitated toward large, liquid markets like Nigeria and Egypt, though country-specific fiscal policies ultimately drove individual bond price movements.

Nigeria

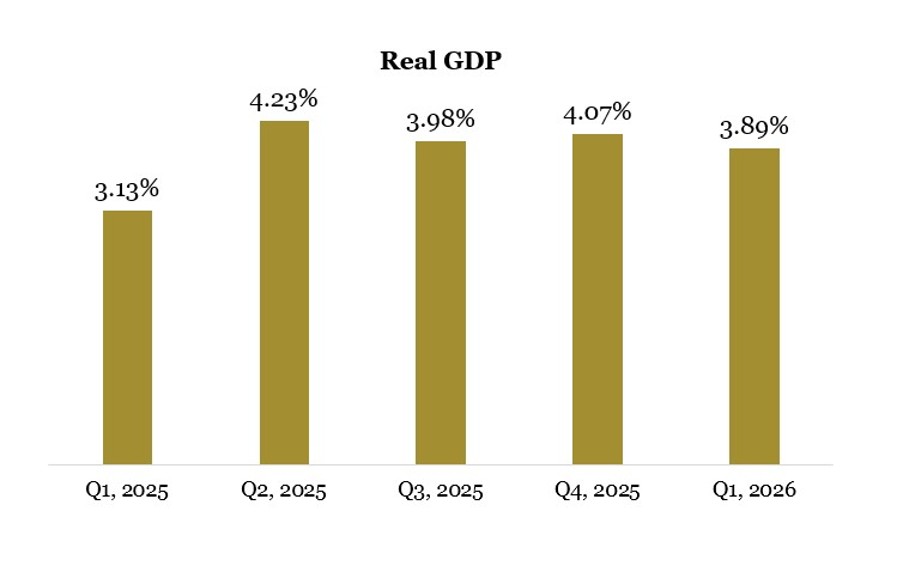

Nigeria’s macroeconomy stabilized in Q2. Inflation ticked up to 15.93% in May due to supply shocks, prompting the central bank to hold its policy rate steady at 26.50%. The naira consolidated near 1,390 per US dollar, while foreign reserves grew to 49.6 billion dollars. In secondary Eurobond markets, Nigeria’s yield curve saw mild volatility, with the long end trading in the high-7% to low-8% area.

Ghana

Ghana’s consumer price disinflation continued, with annual CPI printing at 3.4% in April. The Bank of Ghana kept its benchmark policy rate unchanged at 15.50%, noting stable inflation and reserves near four billion dollars. The cedi appreciated to 11.3 per US dollar, supported by external IMF inflows. In Eurobonds, Ghana’s curve tightened, with the 2026-2032 maturities leading a rally into the low-to-mid teens.

Kenya

Kenya’s headline inflation stayed inside its target band, printing at 6.68% in May. The central bank held its benchmark rate steady at 8.75% in June, maintaining a mild easing bias. The shilling traded stably near 129 to 130 per US dollar, backed by 8.4 billion dollars in foreign reserves. In sovereign Eurobonds, Kenya executed a successful 2.25 billion dollar dual-tranche liability management issue.

Angola

Angola’s disinflation advanced rapidly, with CPI falling to 10.9% in May. This slide prompted the central bank to cut its benchmark policy rate by 50 basis points to 17.00%. Strong oil revenues expanded national foreign reserves to 15.5 billion dollars, while the kwanza stabilized at 919 per US dollar. Angolan Eurobonds responded positively; secondary yields dropped 50 to 70 basis points over Q2.

Egypt

Egypt’s urban inflation slowed gradually to 14.6% in May. The central bank held its benchmark deposit rate steady at 19.00%, citing regional geopolitical conflicts and lingering commodity market risks. The currency remained stable near 30.5 per US dollar, while total foreign reserves reached 39 billion dollars under IMF backing. In Eurobonds, Egypt launched a successful 1.0 billion dollar eight-year social bond at 7.625%.

Q3 2026 Outlook

Local market

Looking ahead to Q3 2026, we expect the upward trajectory in yields to persist in the near term, as the DMO has signaled increased domestic borrowing needs. We anticipate the ample liquidity to persist, owing to OMO/NTB and Coupon inflows, thus expecting inflation dynamism, intermitted market volatility and Monetary policy decisions to direct investors liquidity placements.

Eurobond market

Global: We expect one 25 basis point Federal Reserve rate cut if labour softens, while Sub-Saharan credit spreads remain stable on ongoing foreign portfolio inflows.

Nigeria: Disinflation remains key. If headline CPI drops, the central bank might cut interest rates slightly by year-end while the naira exchange rate remains stable. We also look forward to the Eurobond issuance.

Ghana: Additional monetary rate cuts remain possible if the domestic cedi currency holds steady.

Kenya: Subdued domestic consumer prices give room for modest monetary easing, but secondary Eurobond market performance hinges tightly on upcoming new budget fiscal discipline.

Angola: Rapidly lower inflation allows another policy rate cut. Healthy crude oil revenues cushion the macro fiscal outlook, keeping sovereign credit spreads tightly compressed.

Egypt: The Egyptian central bank will likely hold rates until the next scheduled IMF review. Successful domestic subsidy reforms will gradually compress secondary credit spreads.